The purpose of this thread is to discuss macroeconomics and the financial markets. It will cater towards longer-term fundamental based traders, but everyone is welcome to participate.

Self-sufficiency is the greatest of all wealth. - Epicurus

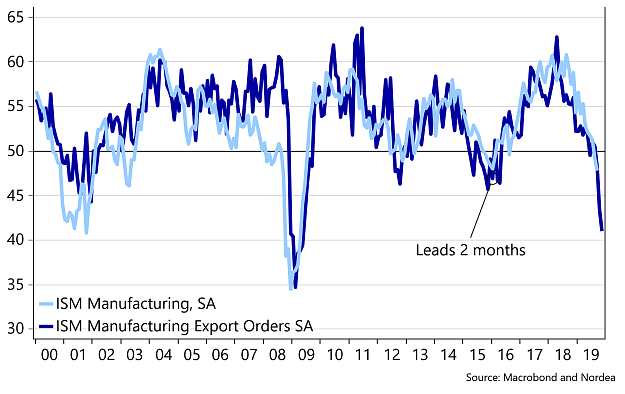

Manufacturing suggest the US is on the verge of recession. Yesterday I shared this chart in another thread:

Attached Image

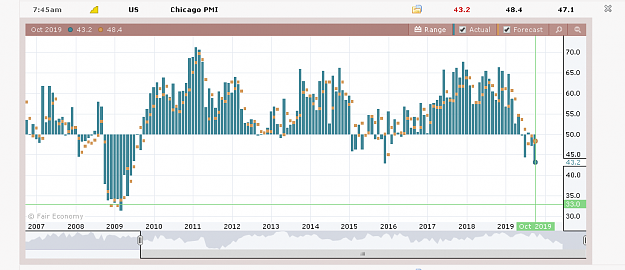

ISM Manufacturing Export Orders is a leading indicator for ISM Manufacturing and its showing something reminiscent of a recession. Today, Chicago PMI (a leading indicator for ISM PMI) came out well below expectations at 43.2:

Attached Image (click to enlarge)

ISM comes out tomorrow and it'll probably be pretty bad judging from the above.

Self-sufficiency is the greatest of all wealth. - Epicurus

Looking at my various indicators 80% of them are bearish I am still waiting for my main one to point south but but even that's not great. There is an interesting article in Reuters https://www.google.com/amp/s/uk.mobi.../idUKL8N27G47J

Ignored

Good article, thanks for sharing Fader123!

If you don’t mind me asking, what is the main indicator you’re waiting to turn south?

Self-sufficiency is the greatest of all wealth. - Epicurus

Unfortunately, I am not at liberty to disclose - due to signing an NDA.

But it's related to related to risk and growth

The issue with indicators they are just that and there are many things that drive the S&P

But there are other indicators/data that I can talk about that are very useful.

Obviously, yield curves (inversion) being one.

These have been discussed elsewhere that have been used to predict recessions

Looking at these directly;

3M and 10y - inverted for 5 months this year with the exception of about two weeks in July

3M and 5y has been inverted since March - and is only just now back to normal

2y and 10y only been inverted for a few days in August-September

Unfortunately, I am not at liberty to disclose - due to signing an NDA. But it's related to related to risk and growth The issue with indicators they are just that and there are many things that drive the S&P But there are other indicators/data that I can talk about that are very useful. Obviously, yield curves (inversion) being one. These have been discussed elsewhere that have been used to predict recessions Looking at these directly; 3M and 10y - inverted for 5 months this year with the exception of about two weeks in July 3M and 5y has been...

Ignored

The yield curves certainly paint a negative macro picture. A lot of people have rejoiced that they've turned positive, but historically turning positive hasn't been a good thing. I still don't fully trust the yield curve though, it's failed to forecast recessions in other nations and the sample size for US recessions is small.

You make a good point about Trump and trying to avoid a recession. As it stands the US is already forecast to add a lot of fiscal stimulus next year so that could push back a recession. Right now my base case is recession, but I'm going to have to try to disprove it and this will be one factor I look at.

Also, totally understood on the NDA. I wouldn't say anything under those circumstances either.

Self-sufficiency is the greatest of all wealth. - Epicurus

Btw Fader123, in addition to the yield curves the Eurodollar futures curve is a very good one to watch. It inverted way back on May 29th, 2018, well ahead of the yield curve. Unfortunately there's not a lot of material written about it, but I understand it has an exceptional track record too.

Self-sufficiency is the greatest of all wealth. - Epicurus

{quote} The yield curves certainly paint a negative macro picture. A lot of people have rejoiced that they've turned positive, but historically turning positive hasn't been a good thing. I still don't fully trust the yield curve though, it's failed to forecast recessions in other nations and the sample size for US recessions is small. You make a good point about Trump and trying to avoid a recession. As it stands the US is already forecast to add a lot of fiscal stimulus next year so that could push back a recession. Right now my base case is recession,...

Ignored

Hi EF5

According to the chap that discovered the yield curve inversion in 1986 he has said that its 7/7 in the US.

I believe he was looking at the 3mth -10 year curve as opposed to the 2s10s that is more commonly used.

Looking at the Feds position there is talk of QE lite and that it is the expansion of the balance sheet that has got traders attention.

In respect of the dollar index - its looks as though a further drop is not out of the question. This could make US equities more attractive

Obviously, timing of the recession is an issue but the implication of a 1 year gap between inversion and recession, QE lite, a cheaper dollar (for overseas investors), Trump going all out (we think) to avoid recession for the time being would put me off going short.

However, when these PMIs and yield curves play out - it should be fun

{quote} Hi EF5 According to the chap that discovered the yield curve inversion in 1986 he has said that its 7/7 in the US. I believe he was looking at the 3mth -10 year curve as opposed to the 2s10s that is more commonly used. Looking at the Feds position there is talk of QE lite and that it is the expansion of the balance sheet that has got traders attention. In respect of the dollar index - its looks as though a further drop is not out of the question. This could make US equities more attractive Obviously, timing of the recession is an issue but...

Ignored

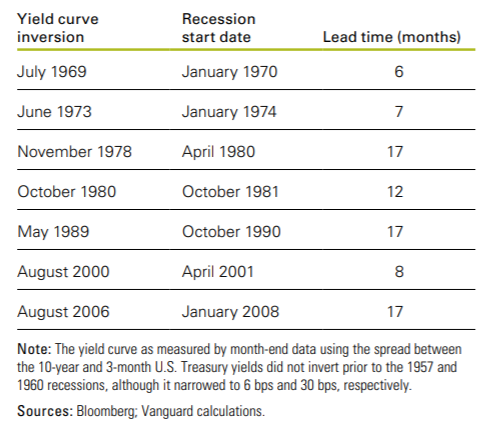

It's too bad the yield curve isn't more precise on timing. Here's a table showing the recession lead time on the 3m-10y curve:

Attached Image

The 3m-10y curve first inverted on March 22nd, 2019 so based on the above chart our recession could start anywhere between September 2019 and August 2020. That's broadly in-line with what I'm expecting.

Self-sufficiency is the greatest of all wealth. - Epicurus

I've shared this elsewhere before, but housing is a leading indicator of the economy and it's remarkable how well everything has fallen into place since the housing peak.

It's no sure thing that we get a recession next year, but the stars seem to be aligning for it. This is my base case and when I get some time I'll attempt to disprove it. (Failing to disprove is more effective than attempting to prove.)

Self-sufficiency is the greatest of all wealth. - Epicurus

I'm going to do an exercise where I posit a hypothesis, explain my reasoning, and then attempt to disprove it. If I can't disprove it I'll assume I'm correct, if I can disprove it I will have been wrong but I'll avoid making a costly trading decision.

This exercise takes time so please pardon me if it takes a few days to get through.

Self-sufficiency is the greatest of all wealth. - Epicurus

Hypothesis: A global recession will start by the end of June 2020.

Supporting Evidence

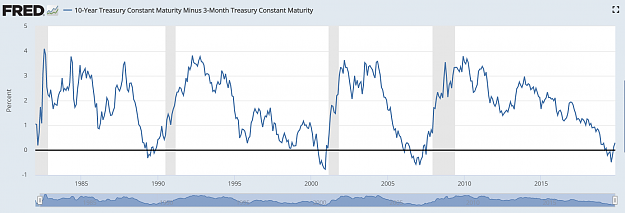

1. The Yield Curve inverted in 2019 which preceded all modern recessions.

Attached Image (click to enlarge)

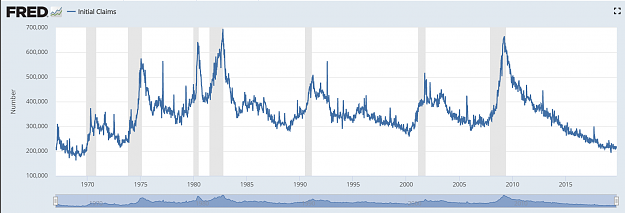

2. Initial Jobless Claims have stopped declining.

Attached Image (click to enlarge)

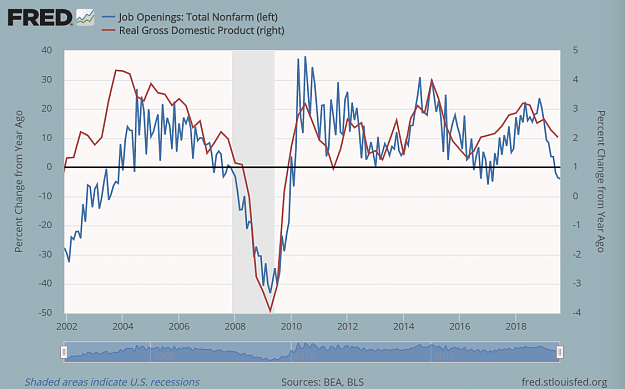

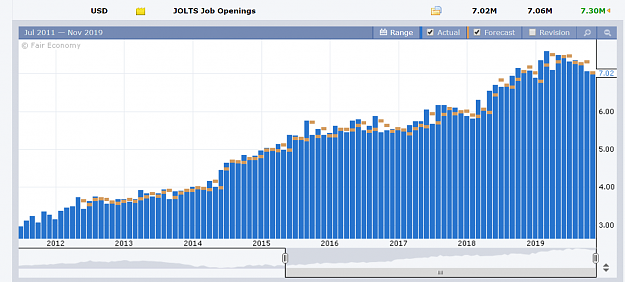

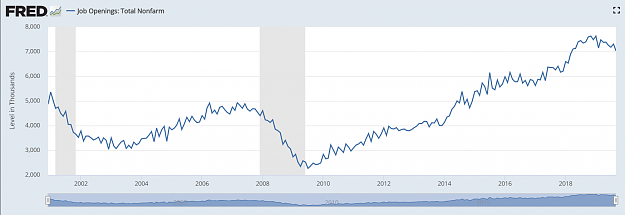

3. Job Openings have trended lower.

Attached Image (click to enlarge)

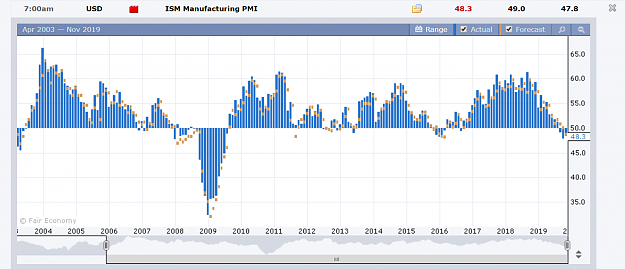

4. ISM Manufacturing PMI is below 50.

Attached Image (click to enlarge)

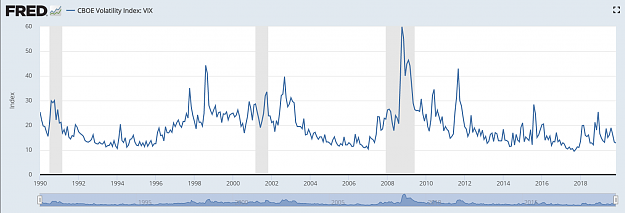

5. The VIX bottomed in 2017.

Attached Image (click to enlarge)

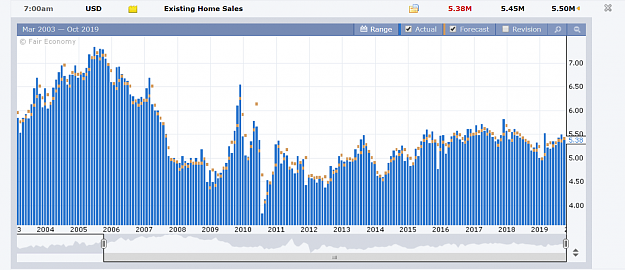

6. Existing Home Sales peaked in 2017.

Attached Image (click to enlarge)

Contradictory Evidence

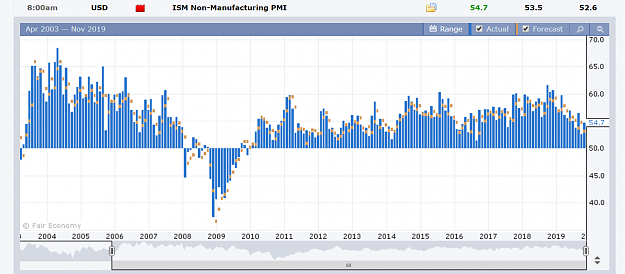

1. ISM Services PMI is doing relatively well. (Services represents a much larger share of the economy than Manufacturing.)

Attached Image (click to enlarge)

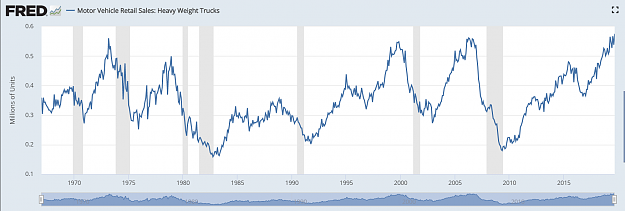

2. Heavy Weight Truck sales haven't turned down.

Attached Image (click to enlarge)

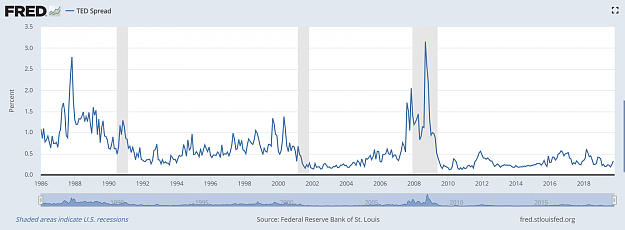

3. TED Spread isn't indicating any financial stress.

Attached Image (click to enlarge)

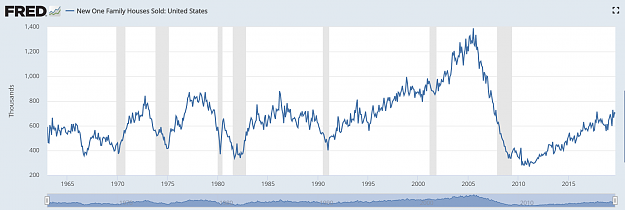

4. New Home Sales have recently hit new cyclical highs.

Attached Image (click to enlarge)

Reasons I may be wrong

There is no solid case for a recession. There's no housing bubble or tech bubble about to collapse this time so what's the trigger? Does there need to be a trigger?

Fed has cut the target Fed Funds Rate 3x and started QE lite.

The US is expected to provide a fiscal stimulus in the near future.

2020 is an election year and Trump may do whatever it takes to postpone a recession.

Housing may provide an economic tailwind if it makes a new leg higher. Higher prices could come as a result of lower mortgage rates.

In future posts, I'll explore the reasons I could be wrong in more detail.

Self-sufficiency is the greatest of all wealth. - Epicurus

There is no solid case for a recession. There's no housing bubble or tech bubble about to collapse this time so what's the trigger? Does there need to be a trigger?

Fed has cut the target Fed Funds Rate 3x and started QE lite.

The US is expected to provide a fiscal stimulus in the near future.

2020 is an election year and Trump may do whatever it takes to postpone a recession.

Housing may provide an economic tailwind if it makes a new leg higher. Higher prices could come as a result of lower mortgage

...

Ignored

There is no solid case for a recession. But there's no solid case for continued growth either. The trend of the data is pointing to a slowdown. It's been a little overshadowed because of Germany and China's issues. The slowdowns elsewhere may be a little deeper than in the US. Maybe we don't go into a recession. But we are long overdue for a correction.

The stock buyback programs have inflated the heck out of the stock market. 20 years ago companies used to spend on research and development. Now, it's all about how much money they can pump back into the stock, increase the stock price, and secure the CEOs job.

The Fed hasn't left much room if we do need to cut rates aggressively. This could greatly exacerbate a downturn. If QE ever becomes the main instrument or tool the Fed uses to calm markets, we may be headed towards a liquidity trap.

Housing isn't going to come down like it did in the last recession. The wealth effect is too important to maintain because of how dependent our economy is on consumers feeling they have the money to spend, and keep spending.

It's the stock market that's going to see a pretty drastic correction. I'm not sure when. These rate cuts could push it back. It's amazing to me that there's investors, money managers, etc that have 10+ years experience and have never experienced a correction. A lot of them probably don't believe it's coming. The rest have no idea what they're in for.

One thing I noticed after what seemed like some 'irrational exuberance' after today's ISM Non-Manufacturing PMI was the trend of the data. The highs keep getting lower and it's looking like we are trending towards contraction numbers.

There is no solid case for a recession. But there's no solid case for continued growth either.

Ignored

One thing I need to explore is whether or not there really needs to be a case for a recession. You could easily point to a culprit for the past two recessions; the real estate bubble and the tech bubble. The early 90s recession was more of a confluence of factors between the savings and loans crisis, high interest rates, high oil, etc. A 2020 recession may resemble that where you could point to the trade war, somewhat restrictive monetary policy, political tensions (UK, Hong Kong), etc.

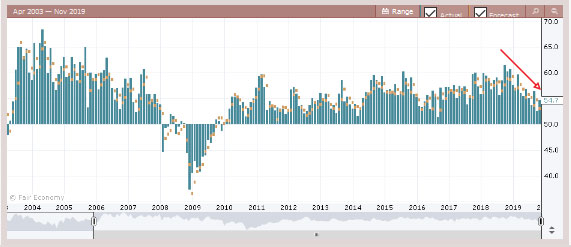

One thing I noticed after what seemed like some 'irrational exuberance' after today's ISM Non-Manufacturing PMI was the trend of the data. The highs keep getting lower and it's looking like we are trending towards contraction numbers. {image}

Ignored

The trend lower in Services PMI is a good point you bring up. It's still expanding, but at a slower pace so definitely not headed in the right direction.

Self-sufficiency is the greatest of all wealth. - Epicurus

In economics, something called a "liquidity trap" was first imagined by a bloke whose name was Keynes. Much of his stuff has been utterly misused and misunderstood. Not for discussion. What he did say was

"There is the possibility...that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest. But whilst this limiting case might become practically important in future, I know of no example of it hitherto."

Well, that was 1936, so my bolding in that quote. It has subsequently been formulated in elegant models by monetary economists (who say there is no "trap" as long as some interest rate is positive), who you don't hear much from these days anymore, least not from central banks. "Real" economists look at the causes, in this case, debt. Central banks cause debt. The media and financial publications (and dare I say it, traders) look to "news". That is what you can see, the effects, like the tip of an iceberg.

I personally have not seen any much mention of robust economics in recent years, despite it being so obvious to me that much of the free world is stuck in a liquidity trap, even by strict monetarists definitions.

North America has negative real interest rates (ie, after any inflation).. Also, I don't think that it is widely known or understood that much of Europe (I'm not exactly sure how you define Europe these days) has had negative nominal interest rates for quite some time - when they lower rates, it is from a negative number to a lower negative number.

This makes a discussion of the yield curve rather awkward, although the media seem to love it.

More than any geo-political stuff going on in the news, this reference by Keynes to "cash" now means, amongst other things, gold and bonds. He was incorrect in saying that debt/bonds would not be desired - it just exacerbates monetary policy impotence all the more in losing control over interest rates.

Not much is said about the current Fed quantity easing, by the way, as they are doing it by stealth - repos and so on. I understand that QE4 (I've forgotten which number) is gunna happen, although details are sketchy. Bit like kicking a can down the road.

Disclaimer - I have been long copper now for a few weeks. It is used primarily in industry, and is hardly a financial thing. It seems to be drifting up. I'll stay in as long as it continues to do so.

In economics, something called a "liquidity trap" was first imagined by a bloke whose name was Keynes. Much of his stuff has been utterly misused and misunderstood. Not for discussion. What he did say was "There is the possibility...that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest....

Ignored

Excellent post LloydOz! Sorry I'm just getting back to you, I have a newborn that's required most of my attention for the past week.

You make a great point about a liquidity trap, but I'm more optimistic about the potential of monetary policy even at zero interest rates. Something Bernanke said has always stuck with me:

...money issuance must affect prices, else printing money will create infinite purchasing power. Suppose the Bank of Japan prints yen and uses them to acquire foreign assets. If the yen did not depreciate as a result, and if there were no reciprocal demand for Japanese goods or assets (which would drive up domestic prices), what in principle would prevent the BOJ from acquiring infinite quantities of foreign assets, leaving foreigners nothing to hold but idle yen balances? Obviously this will not happen in equilibrium. One reason it will not happen is the principle of portfolio balance: Because yen balances are not perfect substitutes for all other types of real and financial assets, foreigners will not greatly increase their holdings of yen unless the yen depreciates, increasing the expected return on yen assets.

Basically, monetary policy has to be effective because the alternative is central banks could buy every asset in the world. Instead, enough QE will create inflation and inflation alone can boost the economy through increased profits on inventories, reduction of the real value of debt, the wealth effect, and an increased urgency to spend by the public.

Self-sufficiency is the greatest of all wealth. - Epicurus

Yes, well, in the meantime, some prescient quotes from Powell found their way to my newsfeed. Kinda like, I was just sitting here, eating my muffin, drinking my coffee, when I had what alcoholics refer to as moment of clarity....

Powell: Connection Between Monetary Aggregate And Growth Has Gone Away

13 November 2019, 19:08

(MORE TO FOLLOW) Dow Jones Newswires

November 13, 2019 12:08 ET (17:08 GMT)

Copyright (c) 2019 Dow Jones & Company, Inc.

Anyways - hey, Bernanke is a very smart guy, of course. Sadly he is/was rather loose with his analysis and words. I could go through that quote and dissect it. Lets just start with just one word - prices. Of what? See, he doesn't say. Then, assets. Changes the goal posts in mid-stream, and I hate that. Analysis must be focused.

Print Yen? You generally don't seek to buy foreign assets with a suitcase stuffed with bank notes (there are exceptions but we won't go there...). That's not how the vast majority of money and debt is created by central banks.

Australia's current central bank chief is a similar idiot. Beggars belief what is their agenda. Politics and central banks are a definite no-go zone.

Yes, well, in the meantime, some prescient quotes from Powell found their way to my newsfeed. Kinda like, I was just sitting here, eating my muffin, drinking my coffee, when I had what alcoholics refer to as moment of clarity.... Powell: Connection Between Monetary Aggregate And Growth Has Gone Away 13 November 2019, 19:08 (MORE TO FOLLOW) Dow Jones Newswires November 13, 2019 12:08 ET (17:08 GMT) Copyright (c) 2019 Dow Jones & Company, Inc. Anyways - hey, Bernanke is a very smart guy, of course. Sadly he is/was rather loose with his analysis and...

Ignored

Japanese asset prices really needed to go up. So much bad debt for the 89 bubble, higher prices would lift the levereaged loss burden that causes depressions. Anyway, I think it was Krugman who said something like in order to get out of a liquidity trap you need to be credibly reckless with monetary policy. The BOJ has mostly lived up to that, but I don't think everyone (hint ECB) can which is where we might run into problems. Obviously, fiscal policy would work too.

Self-sufficiency is the greatest of all wealth. - Epicurus