How do you make the renko charts immune to this problem? Any takers?

Ignored

As far as I can see my Renko charts do look the same regardless on when they start. I think the point is that Renko charts build their bricks on levels measured from the zero level rather than from the starting tick (if this was your objection).

The objection about testing I did not get. IMHO there is no difference in fidelity comparing to the standard charts (if both constructed from ticks).

How do you make the renko charts immune to this problem? Any takers?

Ignored

Build them starting at 01 tick. 01-02, 02-03, 03-04, 04-03 etc. Renko has no gap, so missing ticks shall be covered with fake to adhere to building rule.

{quote} As far as I can see my Renko charts do look the same regardless on when they start. I think the point is that Renko charts build their bricks on levels measured from the zero level rather than from the starting tick (if this was your objection). The objection about testing I did not get. IMHO there is no difference in fidelity comparing to the standard charts (if both constructed from ticks).

Ignored

That's right indeed. Using a fixed point like zero as a fixed reference to build the renko grid can make your charts consistent but then you have the issue of picking that point and justifying why it is special. If you are making a 10 pip renko chart on the EUR/USD why not pick 0.0005 as the starting point instead of say 0? Using a different reference will lead to a different renko chart. The larger the size of the renko bars the higher the possible number of reference points you can have which can give different charts altogether.

Even with these problem I still favor this solution of establishing a fixed reference point. It is much less complicated than something like the default implementation in the F4 framework which frankly I don't see as even remotely useful. In the default F4 code for renko bars they are always constructed using the first price in the buffer as reference. This makes it practically useless as the renko between two system calls is always different since the buffer is a moving window of price data.

For those guys who are interested in using renkos built with zero as the base reference I coded a function for the F4 framework in C++. The function is based on the addNewRenko included with the framework but does not have the problems I talked about:

The beauty of the above is that it can be called in the same way as the other renko function, so you basically do a simple call like:

Inserted Code

addNewRenkoRatesFromZero(PRIMARY_RATES,2,0.0050);

This builds a renko chart for the main pair you used, the last value you pass is the renko size in price units. The above would be 50 pips for the EURUSD. I thought this function to trade and backtest accurately over OHLC, not ticks, it provides a consistent renko chart since it only relies on already closed OHLC bars to create the renko chart. If you trade only at the close of a given OHLC timeframe, say 5 min, this will give you a consistent renko picture. The renko will not be the same as a renko constructed from ticks, especially if you use a renko size that can often be within the range of the OHLC timeframe you choose, but if whatever picture is drawn will always be the same. The price you pay is that you can only trade at the open of a new OHLC bar since information for the renko is not updated before that bar closes. This avoids the accuracy problems when you create renko bars using OHLC instead of ticks and try to trade between bars.

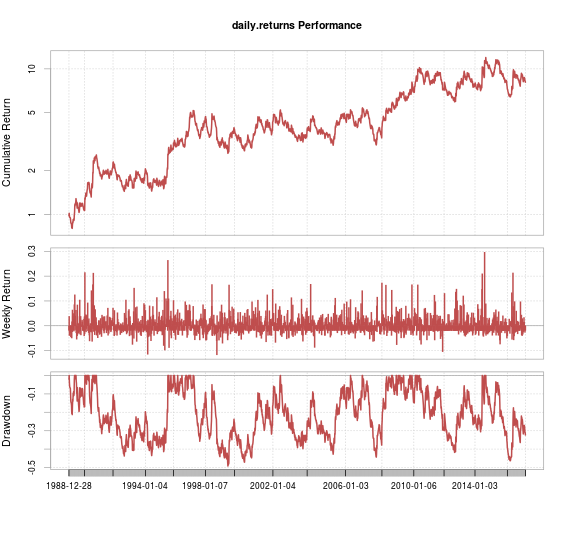

With this I have been able to get some decent machine learning done and my backtests and live trading match as well. Below a visual example of how the renko is created, here a 50 pip renko on the USD/JPY in 2016 data in F4. Renkos built using 5min OHLC. The video shows how it builds as you would expect a consistent renko chart to be built. For each frame F4 rebuilds the renko from scratch using the function I wrote.

I also wanted to say that finding a consistent procedure to create renkos from OHLC was something I had to do since doing renkos from tick data was simply not feasible for me because of the computer power and time it requires. I am happy trading only at 5m bar closes and with this machine learning becomes possible with renko charts for me.

All that I care is that the renko never repaints and that the same OHLC data always shows the same renko bars.

What I have done then is create systems that trade on the 5M in F4 and only trade when a new bar forms on the renko chart. These strategies use STRATEGY_TIMEFRAME=5 in the set file and passedtimeframe=5 on the tester configuration file, they also make use of the renko generating function I posted before. Below and example of such a strategy using a linear regression algo included in F4:

I don't like some of the names the F4 framework has for ML variables, there's no point in calling something learning period/bars used/frontier, etc as these names do not really describe what these variables are. I have decided to call them BARS_IN_FRONTIER, BARS_PER_EXAMPLE and NUM_OF_EXAMPLES which makes more sense IMHO. I also pass the renko size as pips (fourth parameter) and then adjust if it is a JPY symbol by dividing by 100 instead of 10,000. The above code is just a sample, it cannot be used in multi-threaded optimization because I have used a static global variable, something that's not thread safe. I will just use it for a few examples to illustrate some points.

You can even make something like this work with the 60 min timeframe if you use larger renko sizes. The renko function I posted is consistent, so whatever you get, even if there are some "errors" caused by the occasional OHLC bar that will be larger than your renko size, the renko charts will always be the same. The backtests in F4 are still always carried out in OHLC, so we do not miss backtesting accuracy by how we build the renkos as all the creation of the renko timeframe is done within the system code itself.

The ML algo here uses renko bar returns as inputs and uses the MFE/MAE in a fixed renko bar frontier as the output. We can improve on this by also using inputs related to the time between renko bars. This example is just to show that the renkos themselves can give us something useful to start with and it doesn't have to be a smaller renko size using a more complex lower timeframe either.

Using time differences for predictions is not difficult. While you modify the I/O functions you can change the line to use double the number of inputs like this

These would be the mods for the regression_i_simpleReturn_o_mlemse function. It goes without saying that you also need to modify all calls to OHLC values to use the iOpen/iHigh/iLow/iClose functions and use 2, if that's where you're placing the renko array.

When using renkos to train ML algos the data from the returns becomes almost meaningless as we only get info about direction from them. Bars are all the same size so all the ML is getting is which are up and which are down . What we have won by the renko transformation is a lot of information about the timing between these changes, this info is more useful for the ML process. What I wrote before is just the simplest way to include that in ML, use the time diff between renko bars as a type of input. I will post some results we can get with that idea soon.

That said I do use range bars and volume bars (tick volume for spot FX actual volume for stocks). When translating tick data into the data store I use the open and close for the session. In the case of FX Inuse Monday's Sydney open and Friday's New York close.

The rationale for this is that I'm capturing market behavior. My results aren't bad in live trading ... still this logic maybe floored? Thoughts.

Up front disclaimer I haven't used Renko bars. That said I do use range bars and volume bars (tick volume for spot FX actual volume for stocks). When translating tick data into the data store I use the open and close for the session. In the case of FX Inuse Monday's Sydney open and Friday's New York close. The rationale for this is that I'm capturing market behavior. My results aren't bad in live trading ... still this logic maybe floored? Thoughts.

Ignored

How long have you been trading? If you have traded for 4-5 years and it has been working well through all this time then don't change it. If it ain't broke don't fix it. If you haven't traded for this long then you'll have to wait to see enough variation in markets to see whether your assumptions will cost ya.

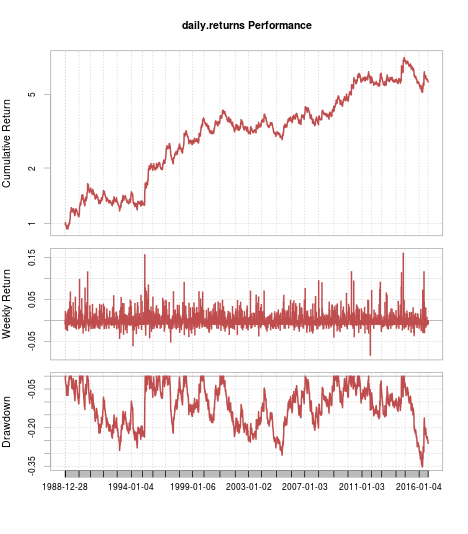

Time differences in renko as ML inputs can lead to some improvements in results. Here is a similar result from USDJPY trading on renko bars derived from 1H OHLC bars (trading only on the 1H open).

{quote} How long have you been trading? If you have traded for 4-5 years and it has been working well through all this time then don't change it. If it ain't broke don't fix it. If you haven't traded for this long then you'll have to wait to see enough variation in markets to see whether your assumptions will cost ya.

Ignored

Well I guess my assumptions are good then ... still the sceptic in me will always questions everything.

Also if you have access to pKantuML you should definitely use it. I presently can backtest 60M, 30Y tests at 0.02 ms per system using my GTX 1080. That's 20K backtests per second.

You can write any custom ML algo you want and just add it in the KantuStrategies.cpp folder in the AsirikuyEasyTrade project and you can search 1000 times faster than if you used only your PC. It's also very good for ensembles. I hate that the source code for pKantuML isn't available however, I'm sure the Asirikuy community could improve the speed of that openCL code even further.

Just as an example I use Lasso regressions, which I added manually since they aren't included in the functions that come with F4. First add the function to AsirikuyMachineLearningCWrapper.cpp:

then add the conditional to call the function in the getKantuSignalML function in this same file (search where the others are defined as well) :

Inserted Code

if (mainKantuMLContainer->g_ml_algo_type[i] == LASSO_REGRESSION){

ensemblePrediction = LZ_Prediction_i_simpleReturn_o_mlemse(mainKantuMLContainer->g_learning_period[i], mainKantuMLContainer->g_bars_used[i], mainKantuMLContainer->g_frontier[i]);

}.

and finally to the write_ml_binaries function in this file as well:

Inserted Code

if (ml_algo_type == LASSO_REGRESSION){

ensemblePrediction = LZ_Prediction_i_simpleReturn_o_mlemse((int)parameter(LEARNING_PERIOD_ML), (int)parameter(BARS_USED_ML), (int)parameter(FRONTIER_ML));

}

Then I can just use ml_algo_type=6 in the pKantuML configuration to mine systems that use a Lasso regression. It's a shame that there's no way to vary ML algo parameters in pKantuML as well (things like the C and gamma in an SVM or the lambda in this lasso example). If you want to use other lambda values besides 1.0 you need to create a new function for each value (a work around I don't like one bit).

If you do R/python then you have to do regular optimizations using a CPU, which takes ages and ages. But if that's your only choice you can do it anyway and just be smarter about what you optimize.

If you modify the I/O functions to use renkos in F4 pKantuML works as well. The only problem is when you use OHLC bars below 15M, it becomes much much much slower. When you go from 60M to 30M it's not just 2x slower but around 3x slower, from 60M to 15M it's like 6x slower and in 5M it's like 20x slower. Maybe memory transfer times between GPU and the Mobo/CPU become too large.

1. From my tests when I use regularization on time series return all the weights become 0 (not relevant consider them noise) and all "EGDE" come from stop loss.

2. From my experiments in last few year the performance of ml mining systems is around +-0 in compare to past data 1987-2012? Regime change ?

How you construct the portfolio from systems ? Do you give more weight to last performance in portfolio?

Hi Algotraderjo, 1. From my tests when I use regularization on time series return all the weights become 0 (not relevant consider them noise) and all "EGDE" come from stop loss. 2. From my experiments in last few year the performance of ml mining systems is around +-0 in compare to past data 1987-2012? Regime change ? How you construct the portfolio from systems ? Do you give more weight to last performance in portfolio?

Ignored

1. What specific regularization? There are many ways to do this. If you have tested in F4 post the specific algo and I'll reproduce.

2. Atm I only trade systems where the performance is positive for the past 3 years and the R is above 0.9 for that period. This besides all the long term filters used in mining. You can find ML systems with those statistics. IMHO one reason why it's hard to get good results in ML is due to that 2013 regime change, if you only look long term then you can get many systems with excellent 1987-2012 performance that have not performed since.