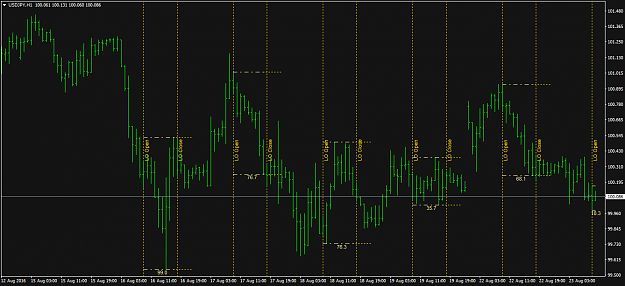

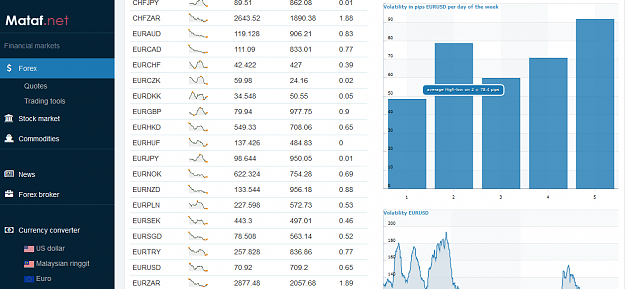

Hello traders! I think we all understand that there is great value in studying market volatility, but it seems our tools for doing so are somewhat limited. What I mean is we have the ATR, ADR, Bollinger Bands, but those studies incorporate information from periods that I really don't trade in like the overnight session and end of US session. Basically our volatility indicators use data from irrelevant time periods and average it in. The result is a more inaccurate prediction of average volatility for the period we might be interested in.

What if there were a measure of volatility that only calculated the average (or median) volatility from a certain time-period of each trading day like the European or the US session. Better yet why not only calculate the average (or median) volatility of that certain period on specific days of the week and month. Better yet why not make it time-period wise highly customizable. You could choose specific hours and a specific day of the week and month.

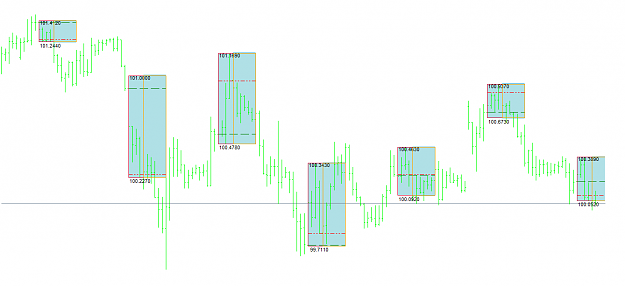

I'm thinking of a customizable indicator that can average (or median) the price range of a selected hourly period in one weekday in every month. For example 7.00-12.00 UTC for every Thursday of every second week of every month. A customizable indicator would let you change the study periods as needed.

Lets say you take a trade from a resistance or support level and need a high probability target that would be met before the end of the session. Such an indicator would give you such a target. Also having such a forecast range would help set a stop loss that is out of the range and thus not very likely to be hit.

I'm not a programmer so I can't create such an indicator, but I think it shouldn't be too hard of a task. Perhaps such an indicator already exists in which case please point me in the right direction.

What if there were a measure of volatility that only calculated the average (or median) volatility from a certain time-period of each trading day like the European or the US session. Better yet why not only calculate the average (or median) volatility of that certain period on specific days of the week and month. Better yet why not make it time-period wise highly customizable. You could choose specific hours and a specific day of the week and month.

I'm thinking of a customizable indicator that can average (or median) the price range of a selected hourly period in one weekday in every month. For example 7.00-12.00 UTC for every Thursday of every second week of every month. A customizable indicator would let you change the study periods as needed.

Lets say you take a trade from a resistance or support level and need a high probability target that would be met before the end of the session. Such an indicator would give you such a target. Also having such a forecast range would help set a stop loss that is out of the range and thus not very likely to be hit.

I'm not a programmer so I can't create such an indicator, but I think it shouldn't be too hard of a task. Perhaps such an indicator already exists in which case please point me in the right direction.