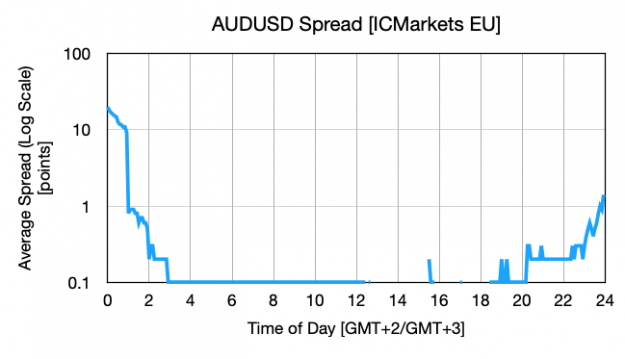

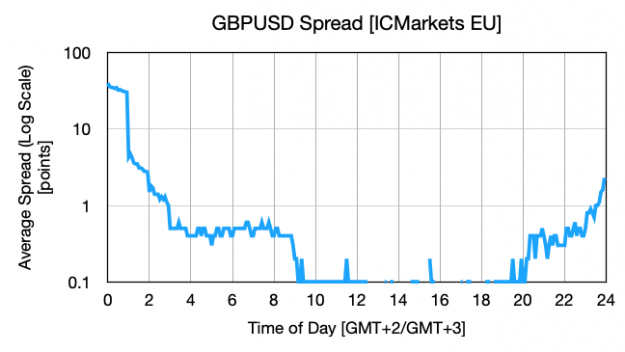

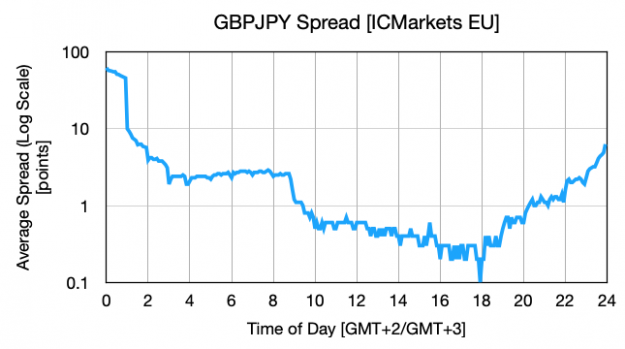

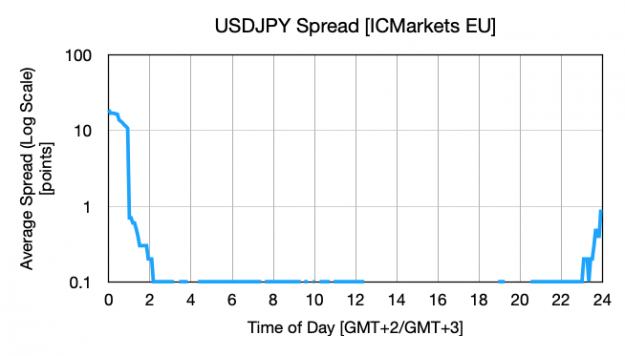

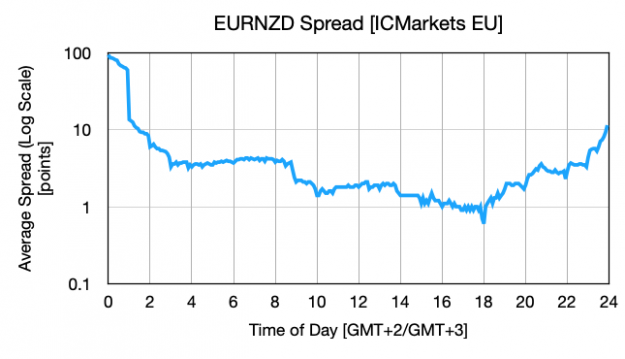

For a recent project I calculated the average spread per time-of-day for several symbols. To my surprise, all symbols showed increased spread around midnight (GMT+2/GMT+3). I expected JPY, NZD and AUD pairs to be traded more during the Asian session, and EUR, GBP, USD more during the London and NY sessions and hence see the maximum spread at a different time of day for these pairs.

Any thoughts on this?

A few examples below (using ICMarkets EU broker data, averaged over the last 4 years):

Any thoughts on this?

A few examples below (using ICMarkets EU broker data, averaged over the last 4 years):

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)