Thank you for this nice post.

I am currently looking to optimize my risk and money management. Could anyone critique it and optimize?

I am conservative but active trader, so I am looking for low draw-down, and using compound interest to increase account with small gains.

Strategy is breakout + trend following on M5 time frame.

Win rate is 49%.

1. Scaling in:

Currently I risk 1% of the account and divide position in two equal parts of 0.5% risk.

When signal to enter has no follow up, I exit position. If there is follow up in next candle I add second position.

2. Scaling out:

I scale out first position when TP is hit: somewhere around 2 times risk (depends on weekly pivots, S/R, price action).

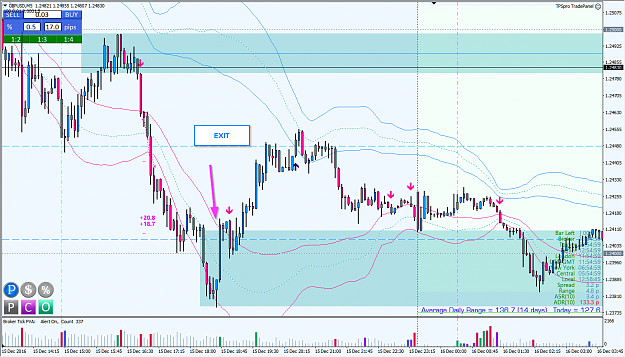

I let the second position run until it breaks 1 standard deviation back of MA50. Like here:

Theoretically it could run into infinity, if trend is sustained. This part must be part of the system to maximize profit on rare occurrences.

I am trying to optimize:

1. Division of the trade. Some are using 2-1-1 (50%+25%+25%). How mathematically calculate which is the best? What is the probability of position running beyond daily ATR?

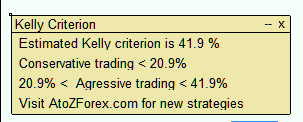

2. Size of the trade. Especially I am trying to use 25% of Kelly criterion. Currently on EUR AUD I have such result:

but 10% is too much for me. Maybe 12.5% of Kelly would be 5% more manageable. EUR or GBP + commodity pairs are trending more than majors.

but 10% is too much for me. Maybe 12.5% of Kelly would be 5% more manageable. EUR or GBP + commodity pairs are trending more than majors.

Please critique the money/risk management so all can benefit.

I am currently looking to optimize my risk and money management. Could anyone critique it and optimize?

I am conservative but active trader, so I am looking for low draw-down, and using compound interest to increase account with small gains.

Strategy is breakout + trend following on M5 time frame.

Win rate is 49%.

1. Scaling in:

Currently I risk 1% of the account and divide position in two equal parts of 0.5% risk.

When signal to enter has no follow up, I exit position. If there is follow up in next candle I add second position.

2. Scaling out:

I scale out first position when TP is hit: somewhere around 2 times risk (depends on weekly pivots, S/R, price action).

I let the second position run until it breaks 1 standard deviation back of MA50. Like here:

Attached Image (click to enlarge)

Theoretically it could run into infinity, if trend is sustained. This part must be part of the system to maximize profit on rare occurrences.

I am trying to optimize:

1. Division of the trade. Some are using 2-1-1 (50%+25%+25%). How mathematically calculate which is the best? What is the probability of position running beyond daily ATR?

2. Size of the trade. Especially I am trying to use 25% of Kelly criterion. Currently on EUR AUD I have such result:

Attached Image

Please critique the money/risk management so all can benefit.

Cut short your losses. Let your profits run on. David Ricardo (1772-1823)