Latency arbitrage trading - a kind of high-frequency trading, the so-called HFT. High-frequency trading algorithms, called HFT, use multiple trading strategies and tactics:

- Rebate trading liquidity (Liquidity Rebate Trading);

- Flash (Flash);

- Pinging dark pools (Dark Pool Pinging) algorithms.

- Trade To delay quotes (Latency arbitrage trading)

When using latensy arbitration is used so-called Colocation (Co-Location). This practice exchange centers, such as the major stock exchanges NYSE Euronext, NASDAQ, BAT and alternative trading systems such as DirectEdge, to lease spaces for HFT, where are your servers close to Exchange servers in order to reduce latency.

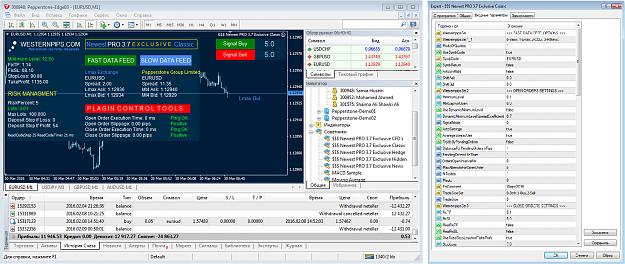

This system was previously available only to large players in the futures market and has never been applied to the forex market. The basic idea is to use a fast data feed (supplier quotes) and find the delay (lag quotes) in the quotes broker terminal Meta Trader 4.

The main task is to search and quick connection provider quotes (fast data feed). To date, there are many contractors that provide access to API / FIX Protocol to market information. But these connections are available only to major market participants - brokers and investment funds.

To date, developed a program Trade Monitor that allows you to get quick quotes Data Feed with 4 largest liquidity providers in the world:

1. Rithmic;

2. CQG FX;

3. Lmax Exchange;

4. Saxo Bank;

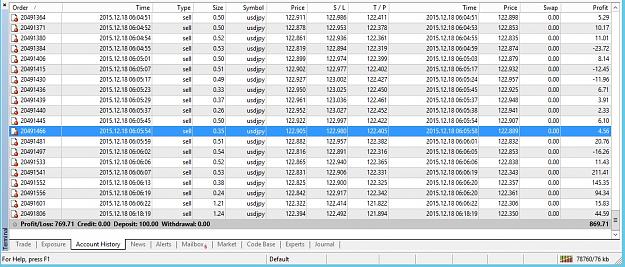

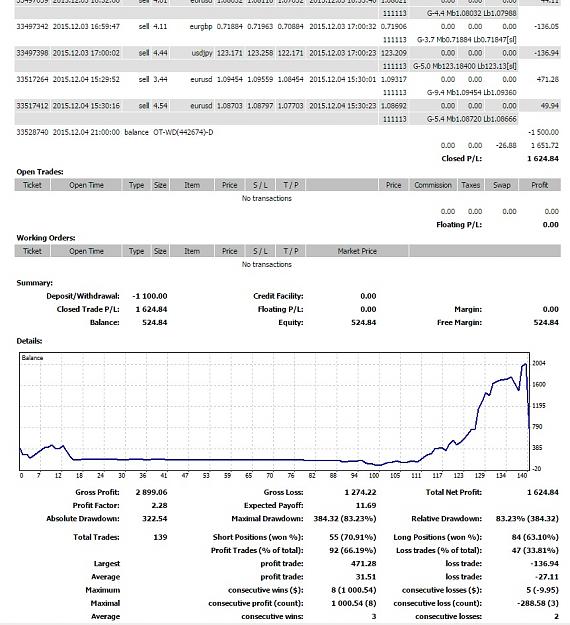

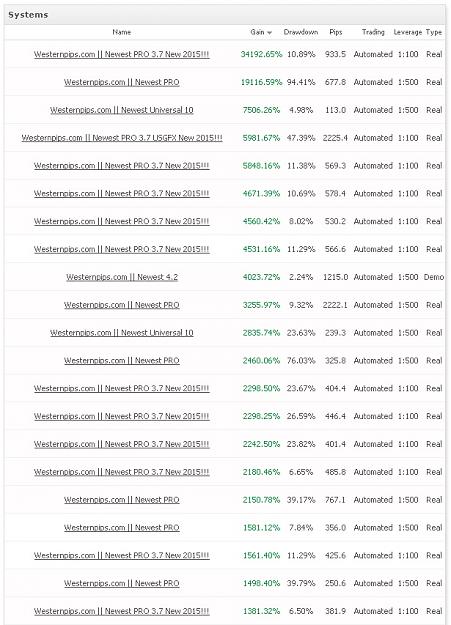

Adviser Newest PRO receives and processes quotes from the program Trade Monitor, looking for arbitrage opportunities.

Next will come to discuss the new version of the program, listen to your suggestions and ideas to fine-tune the system, the introduction of new algorithms and suppliers quotations. Please do not clutter up the theme and negative comments, not pertaining to the topic.

MyFxBook Real accounts monitirings

http://www.myfxbook.com/members/www35

My skype: westernpips.com

Mail: ([email protected])

Web: http://westernpips.com

- Rebate trading liquidity (Liquidity Rebate Trading);

- Flash (Flash);

- Pinging dark pools (Dark Pool Pinging) algorithms.

- Trade To delay quotes (Latency arbitrage trading)

When using latensy arbitration is used so-called Colocation (Co-Location). This practice exchange centers, such as the major stock exchanges NYSE Euronext, NASDAQ, BAT and alternative trading systems such as DirectEdge, to lease spaces for HFT, where are your servers close to Exchange servers in order to reduce latency.

This system was previously available only to large players in the futures market and has never been applied to the forex market. The basic idea is to use a fast data feed (supplier quotes) and find the delay (lag quotes) in the quotes broker terminal Meta Trader 4.

The main task is to search and quick connection provider quotes (fast data feed). To date, there are many contractors that provide access to API / FIX Protocol to market information. But these connections are available only to major market participants - brokers and investment funds.

To date, developed a program Trade Monitor that allows you to get quick quotes Data Feed with 4 largest liquidity providers in the world:

1. Rithmic;

2. CQG FX;

3. Lmax Exchange;

4. Saxo Bank;

Adviser Newest PRO receives and processes quotes from the program Trade Monitor, looking for arbitrage opportunities.

Next will come to discuss the new version of the program, listen to your suggestions and ideas to fine-tune the system, the introduction of new algorithms and suppliers quotations. Please do not clutter up the theme and negative comments, not pertaining to the topic.

MyFxBook Real accounts monitirings

http://www.myfxbook.com/members/www35

My skype: westernpips.com

Mail: ([email protected])

Web: http://westernpips.com

Attached Image(s) (click to enlarge)