- Search Energy EXCH

- 106 Results

-

algoTraderJo replied Jul 21, 2017

algoTraderJo replied Jul 21, 2017This is the cocolizo67 F4 system using an SL with an ATR multiplier: #include "EasyTradeCWrapper.hpp" AsirikuyReturnCode runMondayFridayEA(StrategyParams* pParams) { AsirikuyReturnCode returnCode = SUCCESS; double stopLoss, atr; int ...

1 trade per week system (Backtesting included)

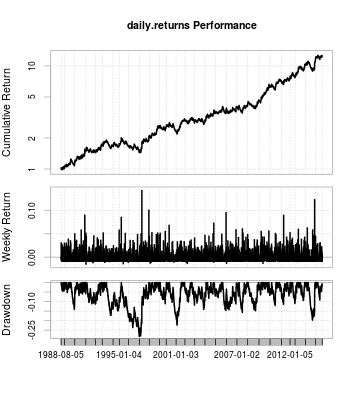

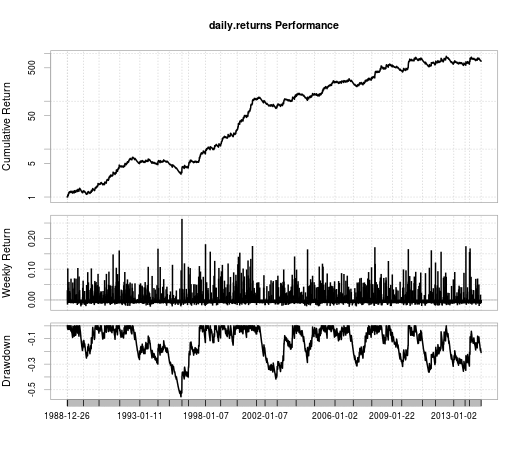

- algoTraderJo replied Jul 19, 2017

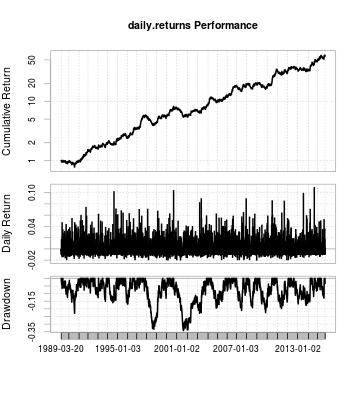

And with a 100 pip stop... image

1 trade per week system (Backtesting included)

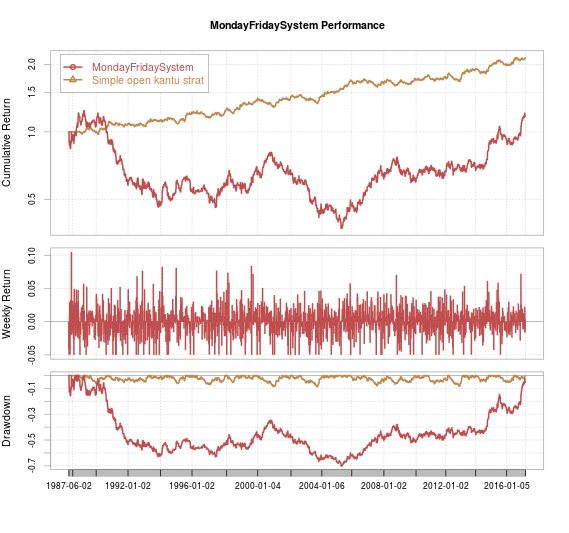

- algoTraderJo replied Jul 19, 2017

I don't post much now (got two kids so time is a bit short) but I LOVE when someone does a quantitative contribution here at ForexFactory (very rare mates). Congrats to cocolizo67 for putting his work here and sharing it with the community. I ...

1 trade per week system (Backtesting included)

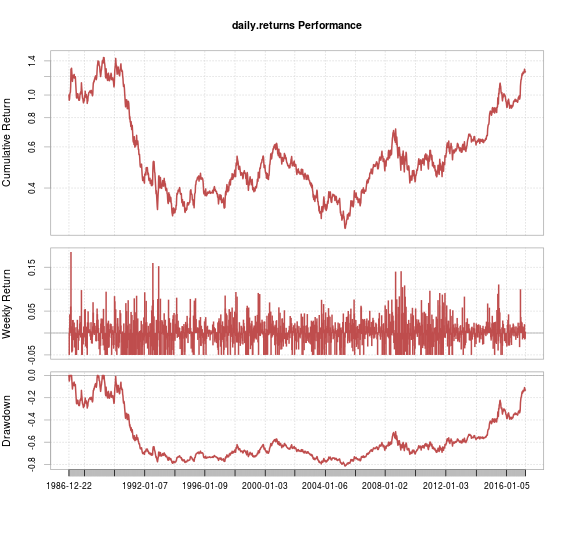

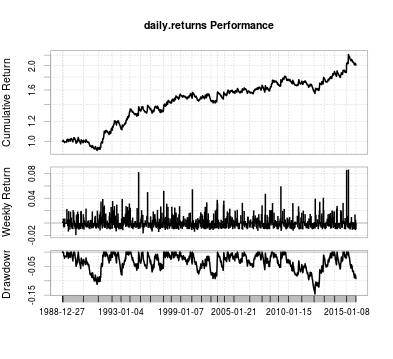

- algoTraderJo replied Mar 29, 2017

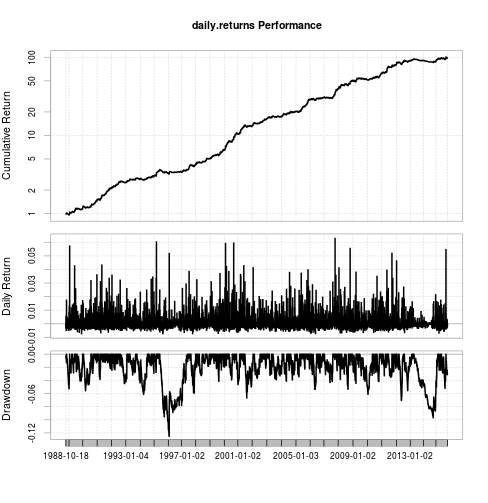

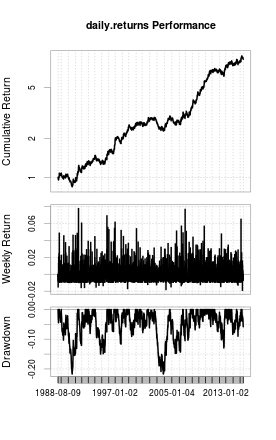

This is an algo I like, it has been trading for a bit more than a year now for me: image It uses a two algo linear classifier ensemble. I post the csv for this system, if anyone wants to explore it more.

Machine Learning with algoTraderJo

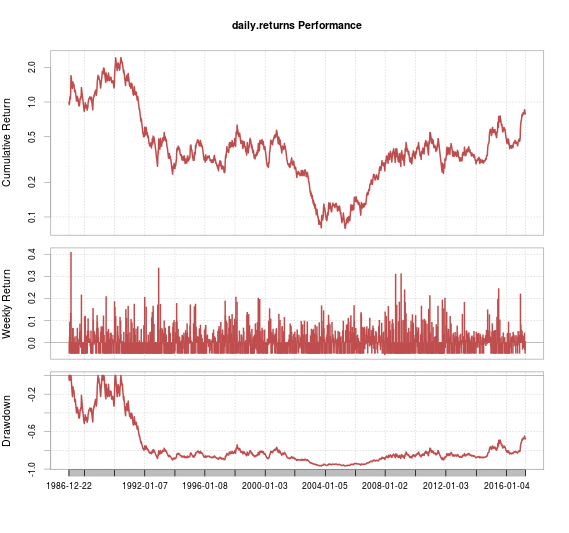

- algoTraderJo replied Mar 15, 2017

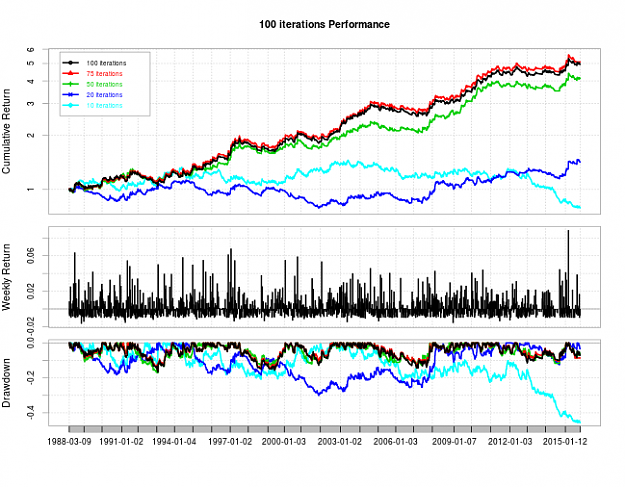

This is what happens when you change the bars used per example with this renko based system. image There is a sweet spot for the BPE between 3 and 5, below or above that we see a performance drop.

Machine Learning with algoTraderJo

- algoTraderJo replied Mar 14, 2017

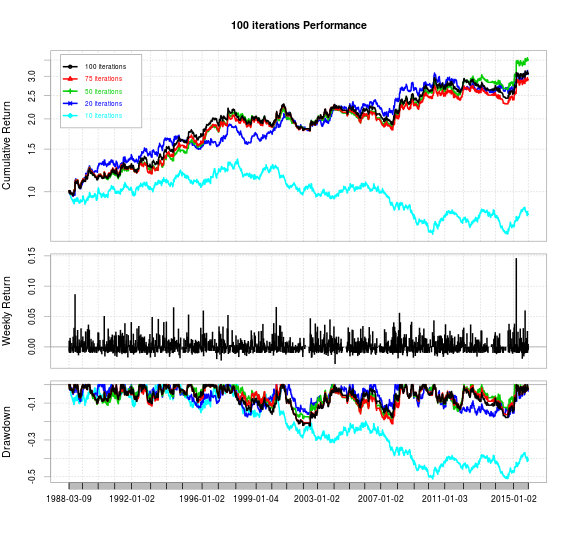

Time differences in renko as ML inputs can lead to some improvements in results. Here is a similar result from USDJPY trading on renko bars derived from 1H OHLC bars (trading only on the 1H open). SL_ATR_MULTIPLIER=1.2 BARS_IN_FRONTIER=60 ...

Machine Learning with algoTraderJo

- algoTraderJo replied Mar 13, 2017

Simple example of USDJPY Linear regression algo using 1H charts and 60 pip size renko bars: SL_ATR_MULTIPLIER=1.3 BARS_IN_FRONTIER=60 BARS_PER_EXAMPLE=2.0 NUM_OF_EXAMPLES=50 RENKO_SIZE_PIPS=60 image The ML algo here uses renko bar returns as ...

Machine Learning with algoTraderJo

- algoTraderJo replied Jan 21, 2016

You can find an example of using pattern filters + hour filtering below. This is the code I used for the creation of the examples: RegressionDataset regression_i_simpleReturn_o_tradeOutcome_examplesByStructure(int period, int barsUsed, int ...

Machine Learning with algoTraderJo

- algoTraderJo replied Jan 21, 2016

I am not using this thread to show you the "best possible system", I am using it to expose new ideas that can help you expand your number of potential ML systems. The pattern based inputs I showed are simply a quick demonstration of the viability of ...

Machine Learning with algoTraderJo

- algoTraderJo replied Jan 14, 2016

I'm gonna show you a simple initial approach to the "pattern detection" idea. I will use the open of the last 7 bars to define a "pattern" which will be the relationships between these values. I then look into the past to see if there are enough ...

Machine Learning with algoTraderJo

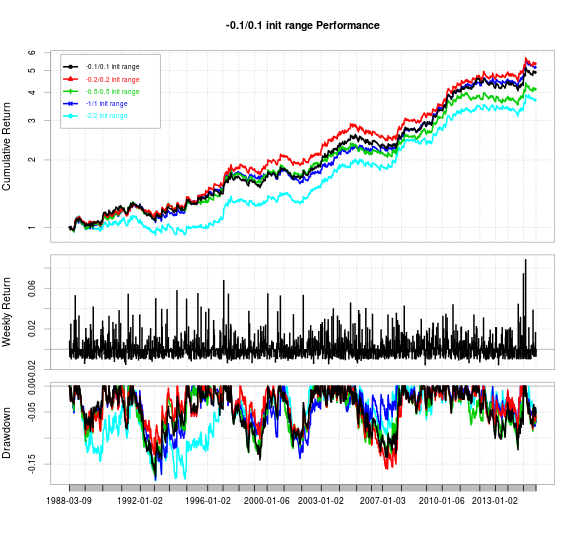

- algoTraderJo replied Nov 8, 2015

Another parameter is the initialization of the random weights when training the NN algo. If you're a good observer and you read the last code I posted you might have noticed that weights in the NN are initialized to random values between -0.5 and ...

Machine Learning with algoTraderJo

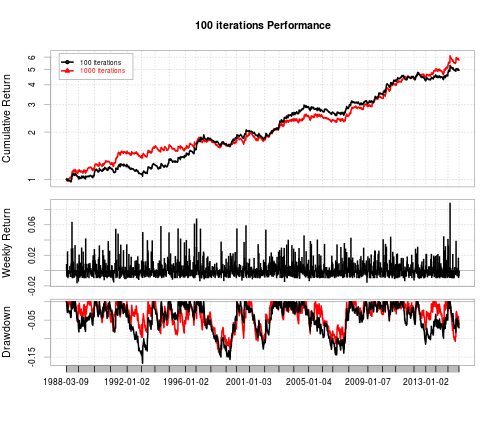

- algoTraderJo replied Nov 7, 2015

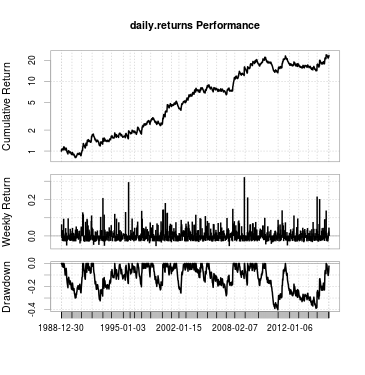

We can also pay a 10x penalty in simulation speed and train for 1000 iterations per NN training, before every trading decision. This would heavily impair DMB analysis. Look how it affects the last posted system. image Is it worth it? You tell me ...

Machine Learning with algoTraderJo

- algoTraderJo replied Nov 7, 2015

Another case on the EUR/USD where the number of returns used to build each example (C parameter) is 5 instead of 2. As in every case retraining of the NN is done before each trading decision. SL = 160% ATR20 A = 1 GMT +1/+2 B = 90 C = 5 D = 90 ...

Machine Learning with algoTraderJo

- algoTraderJo replied Nov 7, 2015

These are some initial sample EUR/USD results using the before mentioned NN function for predictions, the trailing stop as explained before and the input and output structure used for previous linear regression 1H strategies. As in all cases the ML ...

Machine Learning with algoTraderJo

- algoTraderJo replied Nov 6, 2015

I am impressed by all the progress in the cloud enhanced machine learning in Asirikuy. Daniel recently released another 20 or so low DMB systems from these mining experiments. The portfolio has 6 systems on the USD/JPY and 28 on the EUR/USD, all ...

Machine Learning with algoTraderJo

- algoTraderJo replied Oct 31, 2015

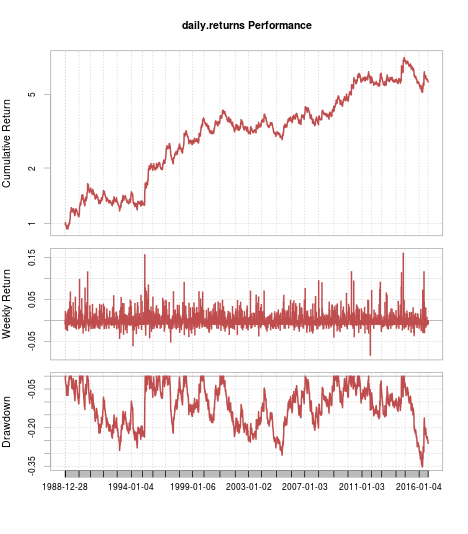

Take a look at this example on the EURUSD 30M timeframe. I am using the last described trailing stop that involves no additional parameters. The machine learning algo is a linear regression which is trained after every trading decision, as I ...

Machine Learning with algoTraderJo

- algoTraderJo replied Oct 6, 2015

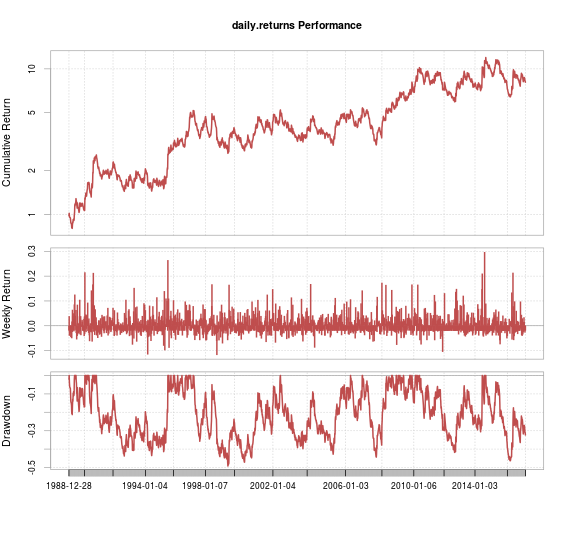

Going down to the 30M timeframe, compounding starts to get really serious. Using the previously described trailing stop based system on the 30M TF we can get the following result (remember that the ML algo is retrained before making each trading ...

Machine Learning with algoTraderJo

- algoTraderJo replied Oct 5, 2015

Another way to attempt to improve your results is to include data from other symbols as inputs. You must be really careful when doing this as you must make sure that the two data sets match perfectly so that you don't get any wrong results due to ...

Machine Learning with algoTraderJo

- algoTraderJo replied Sep 30, 2015

I want to add that the current "Munay" system in the F4 framework contains some nice trailing stop functions that give you a lot of room to explore. IMHO low DMB systems for the GBP/USD can be found using this system if you use the right set of ...

Machine Learning with algoTraderJo

- algoTraderJo replied Sep 27, 2015

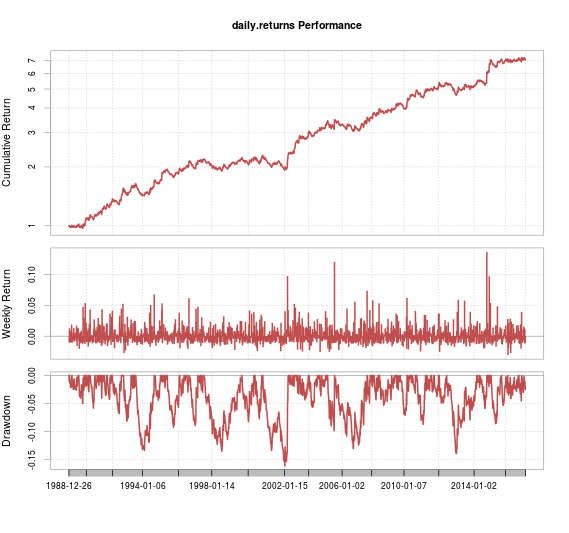

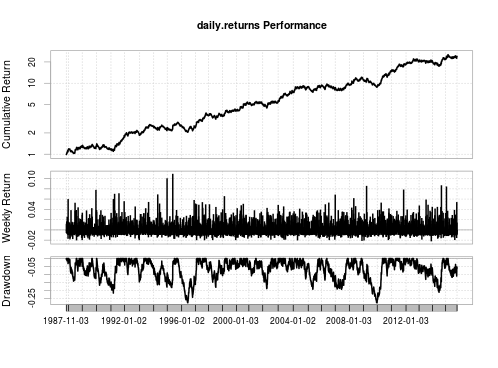

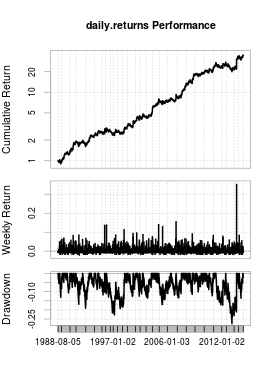

A test on the USD/JPY shows useful potential systems as well. See this one as an example: SL = 90% 1D/ATR20 A= 1 (GMT +1/+2) B= 215 C= 5 D= 100 image I like the lack of additional parameters of this type of trailing. We do not make our DMB search ...

Machine Learning with algoTraderJo