Price growth edges lower despite reasonable economy

Insight

There are rate meetings for the FOMC, Bank of Japan and Bank of England this week, as well as the ECB Forum opening in Portugal tonight.

https://soundcloud.com/user-291029717/lower-inflation-lower-yields-and-lower-rates-a-busy-week-for-central-banks?in=user-291029717/sets/the-morning-call

I’ve got no expectations. But never in my sweet short life Have I felt like this before -Rolling Stones

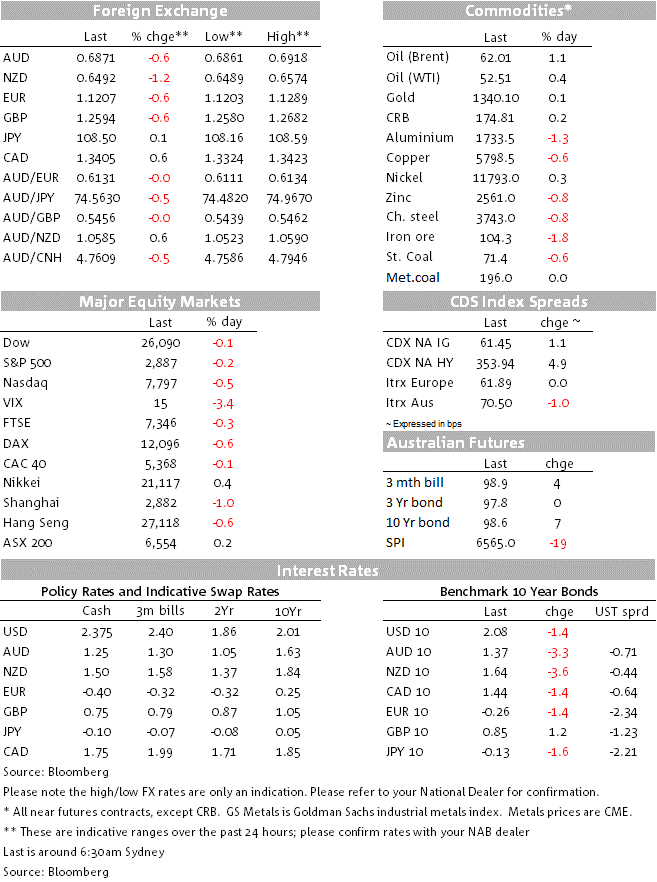

US equities drifted lower on Friday with defensive shares outperforming. US data mostly beat expectations with solid retail sales instigating a pullback on Fed rate cut expectations. The move higher in front end UST yields boosted the USD while softer China data didn’t help commodity linked currencies with the NZD bearing the brunt of it while the AUD ended the week with a 68c handle. Ahead of the ECB Sintra forum that starts tonight, the 5y5y EU inflation swap plumbed to a new record low on Friday and in a similar vein long term US consumer inflation expectations also hit a new record low setting the scene for the FOMC meeting midway through this week.

Late in our session on Friday, China activity readings for May revealed a disappointing set of numbers (details below) with industrial output hitting a 17-year low in May while the rebound in retail sales was likely embellished by a special Labour Day holiday effect. In contrast US data releases were mostly stronger than expected with core US retail sales in particular not only beating expectations, revision to previous months were also solid. Thus the picture is that the US consumer remains in rude health while China’s economic slowdown is becoming more entrenched with stimulatory measures introduced so far unable to stop the rout.

The better than expected US retail sales data boosted front end UST yields, triggering a small unwind of Fed rate cut expectations ahead of the FOMC meeting this week. The UST curve closed with a small flattening bias while the 10y rate ened the week at 2.08%, essentially unchanged on the week.

US Michigan consumer sentiment reading dropped 2.1points to 97.5, near the 98 consensus, but perhaps more importantly the 5-10 year inflation expectations series fell to 2.2%, a new all-time low, from 2.6% in May. This measure has averaged 2.5% in each of the last three years, so the 2.2% reading is material decline and it would be hard to believe this decline won’t be part of the discussion at the FOMC meeting later this week, particularly bearing in mind the stubbornly low US inflation.

Low inflation expectation is also likely to be a theme discussed at the ECB Sintra gathering that starts later today. The EU five-year five forward inflation swap, Draghi’s preferred market inflation reading, hit a new record low of just below 1.12% on Friday. Over the weekend ECB Nowotny said that it’s too soon to draw conclusions from a drop in inflation expectations. Also over the weekend, ECB vice president Guindos noted that the Bank will add stimulus if inflation expectations become deanchored, although he didn’t think this was currently the case citing the stability of other inflation measures such as the survey of professional forecasters.

So against a backdrop of better US data releases and lower inflation expectations, the USD was broadly stronger on Friday with the data outweighing concerns over US inflation. In index terms the USD was stronger across majors ( DXY +0.58 to 97.548 and BBDXY +0.42% to 12002.3) and also against EM and Asia ( EMCI -0.23% and ADXY -0.12%).

Softer China data didn’t help pro cyclical G10 currencies with NZD, AUD and CAD not only underperforming on Friday but also losing ground over the week as a whole. That NZD was the notable underperformer down 1.2% to close the week just below the 0.65 mark. The NZD was out of favour for the whole week, falling every day and down 2.6%, more than reversing the positive daily run over the previous week. It is not often that the BNZ manufacturing PMI triggers a market reaction, but it did so this month after falling to just above the key 50 mark to its lowest level since 2012. The data backs up some of the anecdotes we’re hearing on the ground about a softer economy. GDP data this week is likely to show trend-like growth for Q1 (consensus is at 0.6% q/q), but concerns are setting in about how the economy is currently faring and will track in the second half.

Soft China data and concerns over global growth outlook didn’t help the AUD either with the pair trading down to an overnight low of 0.6861 and now opens the new week at 0.6874. Worth noting too that the AUD/JPY closed the week below ¥75, this cross tends to be regarded as the weapon of choice on risk off events and technically it now looks vulnerable to the downside. Ahead of the G20 meeting and with simmering tension in Middle East and Hong Kong, a lower AUD/JPY could be the trigger for a lower AUD/USD too.

Worth noting too that NAB has changed its view on the RBA cash rate, to include an extra cut in late 2019 (to 0.75%) – while heavily data dependent we have tentatively placed the cut in November. We also think that lower interest rates will be supported by fiscal stimulus later this year. We would not rule out the possibility of alternative monetary action in early 2020, in addition to further rate cuts, if the economy remains very subdued, but have not put it into our projections.

A last word on US equities, the close lower on Friday, but still higher on the week. Looking at the S&P 500 sub-indices performance, utilities, a defensive sector, outperformed up 0.99% while IT was the big loser, down 0.83%. Worryingly as well, the semiconductors sub index, usually regarded as a good leading activity indicator fell 2.46% with Broadcom shares sharply lower on the back of news that the company had reduced its 2019 revenue forecast by $2bn, noting customers are trimming orders because of the trade tensions, including US curbs on sales to Huawei.

Oil prices closed higher on Friday(Brent 1.14%) , after coming under pressure midday through the session. Iron ore closed fell the week at 1.8%, but still closed the week 6.7% higher at $104.3. Gold was little changed after hitting a 14 month high of $1358.26

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.