US GDP growth slows markedly, and inflation remains the focus

US GDP growth slowed to 1.6% annualised in the first quarter of this year, less than half the 3.4% rate recorded in 4Q23, but core inflation was stronger, picking up from a 2% annualised rate to 3.7%. This implies upside risks to tomorrow’s key monthly core PCE deflator and makes a near-term rate cut even less likely

| 1.6% |

US GDP growth1st quarter, 2024 |

| Lower than expected | |

Higher inflation catches the markets' eye, rather than weaker growth

US first quarter GDP growth is an annualised 1.6%, well below the 2.5% consensus expectation, but inflation is hotter with the core PCE deflator up 3.7% annualised versus 3.4% expected. This suggests, assuming no revisions to monthly data, that the core PCE deflator will come in above 0.4% tomorrow rather than the current 0.3%MoM consensus forecast. Unsurprisingly, Treasury yields have pushed higher as if that is the case, it makes a near-term Federal Reserve interest rate cut look even more unlikely.

That said, this inflation number is a quarter-on-quarter annualised measure, so any revisions to October through February could have influenced today's outcome - we won't know until tomorrow when we get the monthly income and spending report. We could still get a 0.3%MoM, but we have to acknowledge that today’s data makes it look less likely.

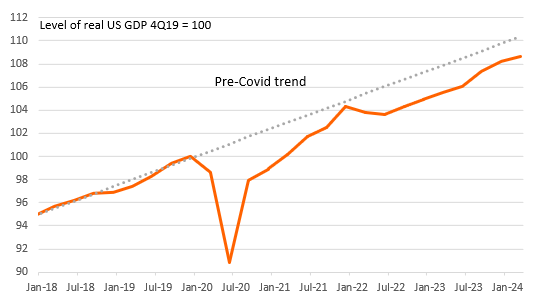

GDP levels versus pre-pandemic trend

GDP still running below pre-pandemic trend levels

In terms of the GDP growth breakdown, consumer spending was softer than thought likely, rising 2.5% annualised, while residential investment was a very firm +13.9%. Business capex was subdued, government spending saw a marked slowdown to 1.2%, while weakness in net trade subtracted 0.9pp from the headline growth rate, and inventories subtracted a further 0.35pp. The chart above shows that while GDP has performed well, the level of output is still a couple of percentage points below where we perhaps could have been had the pandemic not happened, and instead, the economy had continued running at its 2024-19 growth trend.

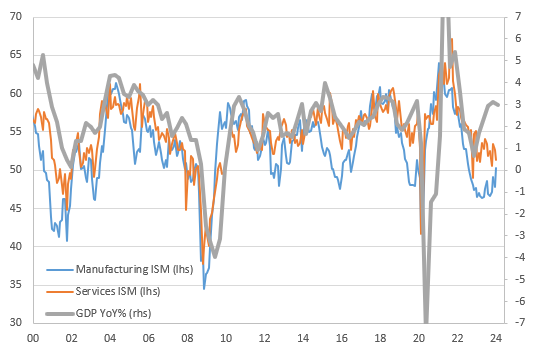

Business surveys are painting a weaker picture than GDP growth

As for the growth outlook, we expect to see more subdued activity in upcoming quarters. The divergence between business surveys and official data is very wide. We strongly suspect that business caution will translate into weaker hiring and wage growth and subdued business capex, and that will eventually show up in the official GDP data. The move higher in market borrowing costs this year will also weigh on activity and eventually dampen price pressures in the economy. Nonetheless, there is next to no chance of a rate cut before September.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more