Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

The S&P 500 Index closed 0.25% higher on Friday, finishing the week 2.5% higher.

Events Round-Up

JN: Tokyo CPI (y/y%), Jan: 4.4 vs. 4.0 exp.

JN: Tokyo CPI x-fr. food, energy (y/y%), Jan: 3.0 vs. 2.9 exp.

NZ: ANZ activity outlook, Jan: -15.8 vs. -25.6 prev.

US: Personal income (m/m%), Dec: 0.2 vs. 0.2 exp.

US: Real personal spending (m/m%), Dec: -0.3 vs. -0.1 exp.

US: PCE core deflator (y/y%), Dec: 4.4 vs. 4.4 exp.

US: Pending home sales (m/m%), Dec: 2.5 vs. -1.0 exp.

US: U. of Mich. consumer sent., Jan: 64.9 vs. 64.6 exp.

I’m stoked on ambition and verve. I’m gonna get what I deserve..Hey, yeah, whoa-ho, I’m on a roll. Ridin’ so high, achieving my goals – Miley Cyrus.

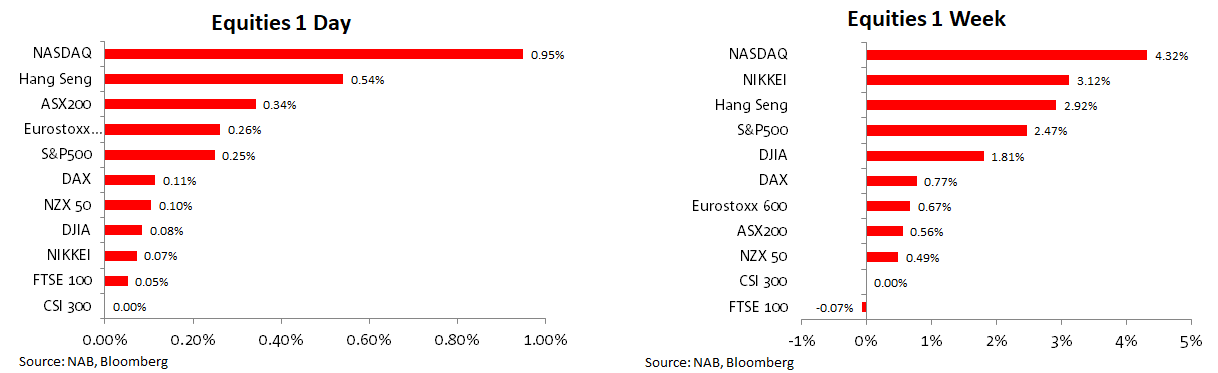

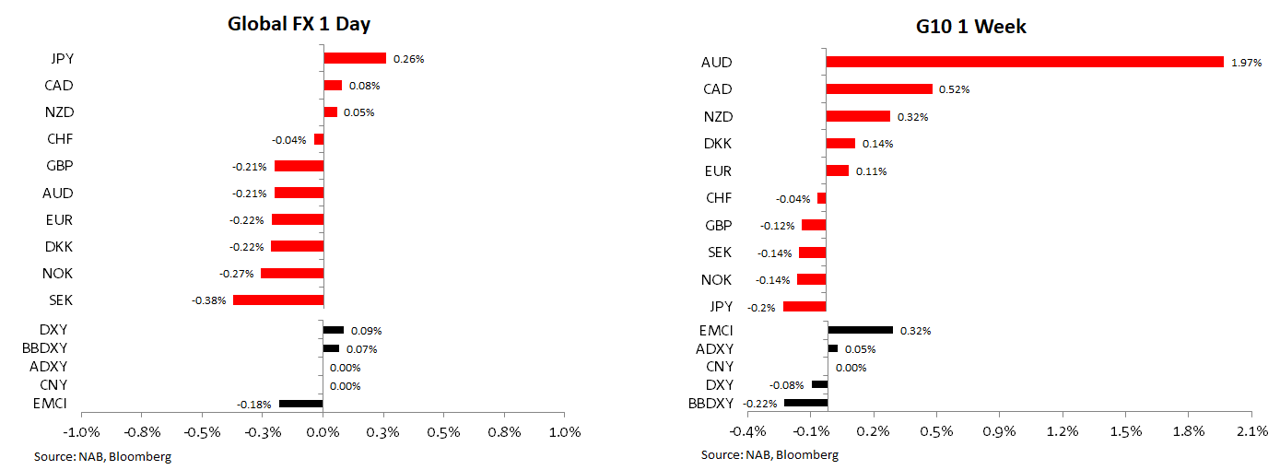

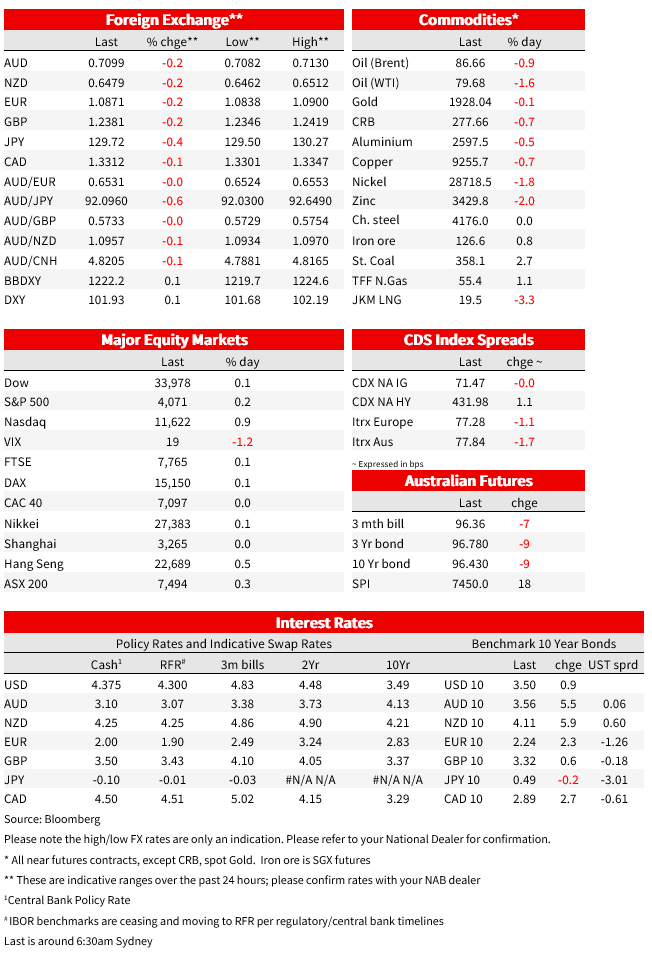

The tech heavy NASDAQ led the gains in US equities again on Friday with the benchmark finishing the week with an impressive roll of four straight weekly gains. Mixed earnings by tech companies have seemingly been trumped by the prospect of an imminent Fed pose. December Core PCE printed in line with expectations but the yoy decline helped cement expectations for a downshift in Fed rate hike this week, UST yields were little changed while domestic yields were the big weekly movers. Quiet end to the week in FX, AUD is the week’s notable outperformer.

The S&P 500 Index closed 0.25% higher on Friday, finishing the week 2.5% higher. Sector performance was mixed on the day with six of the 11 main industry groups ending in the green, consumer discretionary and real estate sectors the top performers. The Nasdaq 100 Index was the outperformer on the day and the week, gaining close to 1% on the Friday and 4.3% on the week. Indeed, the NASDAQ is now on a four-week winning streak, up 11% year to date and on track to record its best January since 1999.

Notwithstanding mixed outcome from tech companies’ earnings reports with Tesla climbing over 3% on Friday following better than expected numbers, there have also been notable underperformers with Intel on Friday joining Microsoft and Texas Instruments revealing a dreary outlook. Intel shares fell 6.4%, the most since September, after the chipmaker issued one of its weakest ever quarterly forecasts as a slump in personal-computer sales hits the business.

Ahead of the ECB this week, European equities were slightly higher on Friday, the Stoxx Europe 600 closed 0.25% on the day and up 0.67% on the week. Thus, marking time ahead of another 50bps hike expected by the ECB this week, but still doing quite well year to date, up 7.13%, outperforming the S&P 500 at 6.02%.

Of note for risk sensitive currencies, such as the AUD and reflecting the positive vibes in the equity market, the VIX index closed the week at 18.5, down two points over the past 5 trading days.

Equities Performance

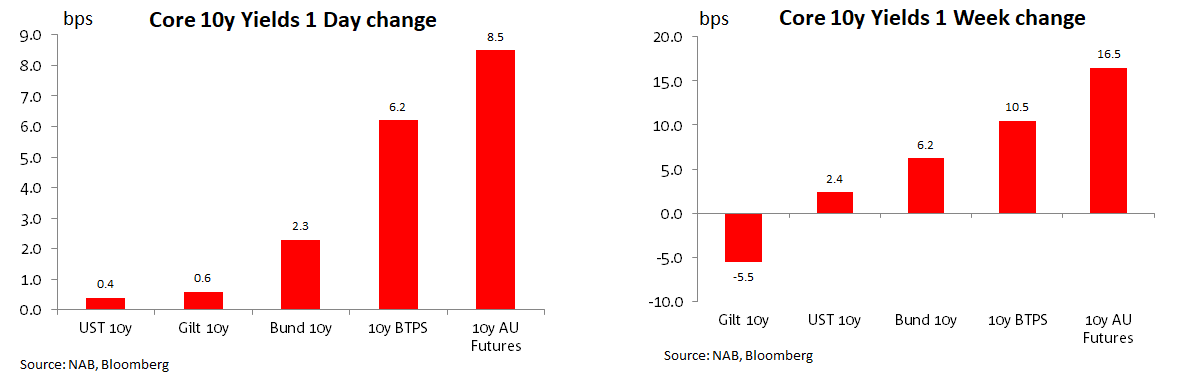

UST yields were little changed on Friday. 10y UST yields ended the week at 3.50%, essentially unchanged on the day and 2.4bps higher on the week. During our APAC session the 10y Note tested levels just above 3.56%, boosted by yet another bigger than expected rise in Tokyo’s CPI.

Consumer inflation in Japan’s capital rose 4.4% yoy in January (4.0% expected) while the core reading also beat rising to 3% yoy vs 2.9% expected. The Tokyo readings are a good leading indicator of the nationwide estimates, and the data flow continues to raise question marks over how transitory Japan inflation really is, reinforcing the view that the BoJ YCC policy has passed its used by date.

The move in UST yields run out of steam during Friday’s overnight session, US data releases revealed a bigger-than-expected drop in real personal spending and a PCE deflator printing broadly in line with estimates. US Real consumption fell 0.3% in December, below the consensus, -0.1% while the core PCE deflator rose 0.3%mom, in line with the consensus. Encouragingly for the Fed, the Core PCE printed 4.4% yoy, the lowest since October 2021, generating a 3-month annualized rate to 2.9% from 3.5%, the lowest read since January 2021. So, the PCE direction of travel should be good news for the Fed. Indeed, a step down to 25bps hike looks well priced this week (OIS market at 26bps taking the Funds rate to a 4.50-4.75% range). The Final University of Michigan’s survey was also out on Friday (64.9 vs 64.4 preliminary) showing a small retreat in inflation expectations, one-year inflation expectations were revised to 3.9% from 4.0%, while 5-to-10 year inflation expectations were revised to 2.9% from 3.0%

Looking at core yields over the past week, Australian counterparts were the notable movers with the 10y Bond Futures climbing 16.6bps to 3.57%, the move largely coming from the stronger than expected CPI print mid-week.

Ahead of the FOMC meeting this week, Former Treasury Secretary Summers told Bloomberg news that the Fed should “maintain maximum flexibility” at the upcoming meeting, not committing to rate hikes and at the same time the possibility of further rate increases shouldn’t be taken off the table.

Over the weekend Fed Whisperer Nick Timiraos from the WSJ noted that the Fed is likely to lift the funds rate by 25bps this week, but a live debate on when to pause is likely given that although we have seen an ease in price pressures, wage data are at odds with concerns that the job market is too tight and the economy is operating above capacity .

Core global yields over the past week

Moving onto FX, it was a subdued end to the week with all G10 pairs moves contained within +/-0.3% range, SEK a small underperformer, down 0.38%. The AUD was 0.21% lower on Friday, but of note it was the outstanding performer during the week, up close to 2% and looking to consolidate a move above the 71c mark ( now trading at 0.7099). After the softer than expected labour report on January 18, which triggered a rally in domestic rates, forcing the AUD down to a low of 0.6876, last week the stronger than expected domestic CPI print, triggered a reassessment of RBA rate hike expectations and a broad move up in Australian yields. This domestic dynamic boosted the AUD with the risk sensitive currency also finding support from the ongoing positive risk sentiment, evident in equity markets.

The kiwi spent most of the day (and week) hovering just under 0.65 and closed the week just under that level. My colleague Jason Wong noted the rainfall in Auckland on Friday night of biblical proportions, with more to come this week, will add both supply-side and demand-side pressures for the region, a source of additional inflation pressure over the months ahead.

Ahead of the Fed, ECB and BoE meetings this week (see more below), the USD was little changed on Friday and a tad softer on the week (BBDXY -0.2%). The Euro lost a bit of ground on Friday (-0.2%) but closed the week comfortably above 1.08 (now at 1.0856) and in line with our expectations for the pair to move into a 1.08-1.12 range over coming months. GBP recorded a similar price action and starts the new week at 1.2381.

FX Performance

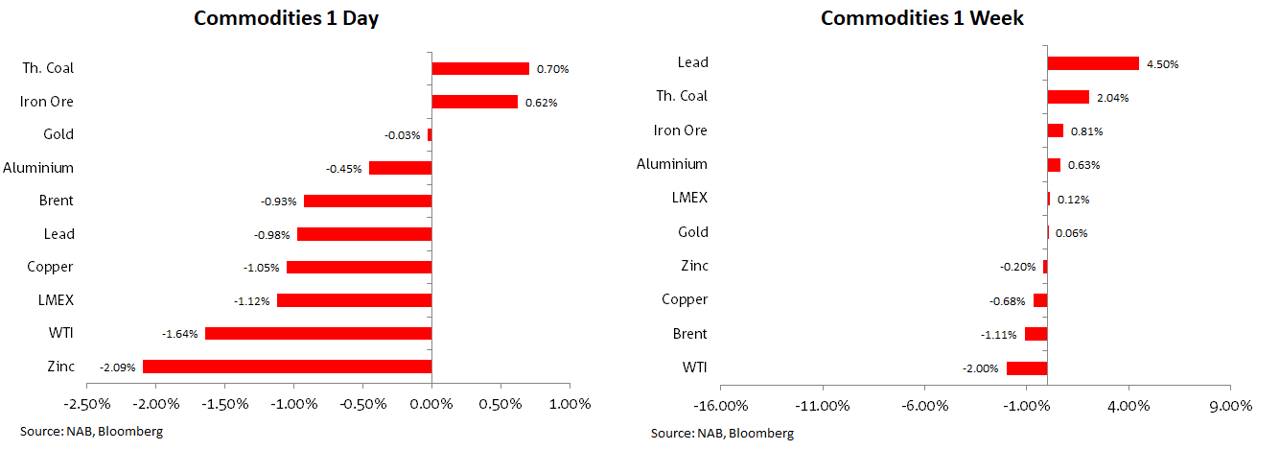

Metal and oil prices were lower on Friday (WTI -1.64%, LMEX -1.12%) while Thermal coal (+0.7%) and iron ore ( +0.62%) managed to edge out small gains. On the week most commodity prices were little changed.

China comes back on-line this week after the Lunar New Year break with the market expecting a decent rebound in activity, especially in the services sector. On Sunday, China reported a sharp drop in new Covid-related deaths during the holiday, somewhat surprising given the increase in travel was likely to result in more infections across the country. China’s CDC said on January 25 that the number of Covid-related deaths and severe cases at hospitals declined by more than 70% from peak levels reached in early January.

Meanwhile in geopolitical news, Bloomberg reports Israel carried out a clandestine drone strike targeting a defence compound in Iran, as the U.S. and Israel look for new ways to contain Tehran’s nuclear and military ambitions, according to U.S. officials and people familiar with the operation.

Commodities Performance

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.