OPEC Gives Tepid Response to Trump's Demand for Lower Oil Prices

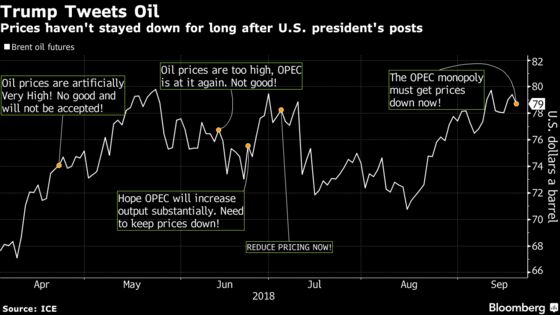

The lack of an immediate response to Trump’s demand adds to speculation about OPEC’s ability to push oil down from $80 a barrel.

(Bloomberg) -- U.S. President Donald Trump’s demand that OPEC take rapid action to reduce oil prices got a tepid response, with the group saying it would boost output only if customers requested it.

In contrast to the dramatic policy U-turn that Trump’s tweets provoked earlier this year, Saudi Arabia, Russia and their allies signaled less urgency and stopped short of promising specific extra volumes of crude.

“Our plan is to meet demand,” Saudi Energy Minister Khalid Al-Falih said after meeting with fellow ministers in Algiers on Sunday. “The reason Saudi Arabia didn’t increase more is because all of our customers are receiving all of the barrels they want.” The kingdom does expect to pump more in September and increase again in October, he said.

The Organization of Petroleum Exporting Countries and its allies are just halfway toward their June pledge to pump an extra 1 million barrels a day of crude to fill the gap created by an economic collapse in Venezuela and renewed U.S. sanctions on Iran. Al-Falih, who openly voiced concerns about the strength of demand and expanding oil stockpiles, said they may only reach that target in two to three months.

The lack of an immediate response to Trump’s demand adds to speculation about the group’s ability, or willingness, to push oil down from near $80 a barrel. It suggests the president’s goal of crippling Iran’s economy through sanctions without significantly raising prices could prove elusive.

"It’s a time of great uncertainty in oil markets, from Iranian output post-sanctions to the global economy and demand,” said Jason Bordoff, director of the Center on Global Energy Policy at Columbia University in New York and a former Obama administration oil official. In Algiers, Saudi Arabia and others have given themselves “the flexibility to respond to changing market conditions."

It’s unclear whether that will be enough for Trump. Brent crude rose above $80 a barrel last week, provoking the U.S. president to direct his first social-media barb against the cartel since July 4. He was returning to a playbook that won him a significant victory in June as OPEC and its allies agreed to roll back production cuts and pump an extra 1 million barrels a day.

Russia followed through on that promise, with recent data showing its production jumped to a new post-Soviet record. Yet Saudi Arabia’s own output actually dropped in July amid signs it couldn’t find enough buyers. Suggestions of record production of near 11 million barrels a day didn’t materialize and the kingdom has hovered near 10.4 million since June.

Saudi Capacity

“Saudi Arabia is uncomfortably squeezed,” said Bob McNally, founder of consultants Rapidan Energy Group in Washington. The kingdom had “limited spare capacity” to compensate for the loss of Iranian supplies, he said.

Demand for Saudi crude could potentially rise to 10.5 million or 10.6 million barrels a day in October, and Al-Falih assured reporters the kingdom could satisfy that by tapping spare capacity. “If demand is 10.9 million barrels a day, you can certainly take it to the bank that we will meet it,” he said.

Still, deepening output losses in Iran and Venezuela meant the compliance rate of OPEC and its allies -- the proportion of their 1.8 million barrel-a-day output cuts achieved each month -- was 129 percent in August, leaving them about 500,000 barrels a day short of their June pledge.

Libya Improves

There was good news from Libya, where oil production has climbed as high as 1.278 million barrels a day, the most since 2013, said Mustafa Sanalla, chairman of the state-run National Oil Corp. If sustained for the whole month, that would be an increase of about 600,000 barrels a day since June, keeping pace with the drop in Iran’s exports over the same period.

Output could go even higher if the security situation improves, Sanalla said, but numerous threats remain. A deadly Islamic State attack on NOC’s headquarters in Tripoli this month “exposes the fragility of security arrangements in Libya,” he said.

Demand Worries

Saudi Arabia is worried about the strength of the global economy, and Al-Falih said there are signs the market is well supplied. “We have topped our storage to the maximum because the demand hasn’t materialized,” he said.

There is a draft framework for OPEC and its allies to continue working together into 2019, which they expect to ratify in December, Al-Falih said. Rapid growth in U.S. production means that oil stockpiles could expand again next year, but it’s too early to say whether the production limits agreed in 2016 would need to remain in place, he said.

Several ministers also offered general commitments to keep markets well supplied, without taking aggressive steps to do so.

Russian Energy Minister Alexander Novak told reporters that his country has the capacity to increase production by several hundred thousand barrels a day in the short term, but using it would depend on the market. The United Arab Emirates has spare production capacity but won’t overuse it, said Energy Minister Suhail Al Mazrouei.

“The Saudis are probably right that market is well-supplied,” Joe McMonigle, an energy analyst at Hedgeye Research, said in a post on Twitter. “But market stability to Trump means lower prices (or at least not higher prices). Mr. Market votes tomorrow.”

--With assistance from Salah Slimani, Javier Blas, Nayla Razzouk, Salma El Wardany and Annmarie Hordern.

To contact the reporters on this story: Elena Mazneva in Moscow at emazneva@bloomberg.net;Wael Mahdi in Kuwait at wmahdi@bloomberg.net;Grant Smith in London at gsmith52@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, Bruce Stanley

©2018 Bloomberg L.P.